Brook Brokers helps property owners refinance commercial real estate in Brooklyn, including multifamily, mixed-use, retail, industrial, and development properties.

Refinancing is typically driven by loan maturities, changes in rates, or the need to reposition debt.

In Brooklyn, refinancing is commonly used when:

Many properties move from short-term financing into long-term loans once performance improves.

Brook Brokers helps property owners refinance commercial real estate in Brooklyn, infii, including multifamily, mixed-usel, imdustrial, and development properties.

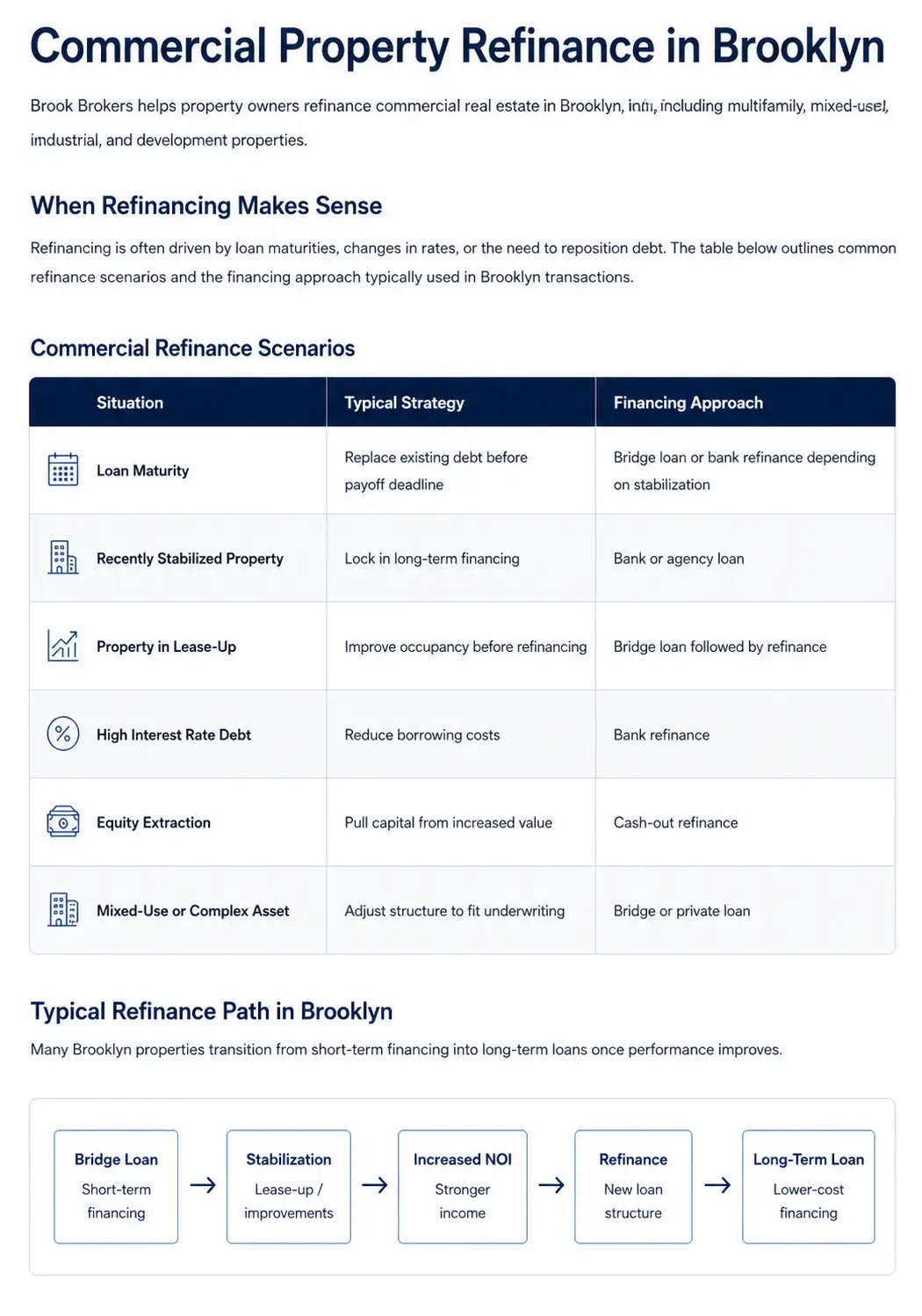

Refinancing is often driven by loan maturities, changes in rates, or the need to reposition debt. The table below outlines common refinance scenarios and the financing approach typically used in Brooklyn transactions.

| Situation | Typical Strategy | Financing Approach |

|---|---|---|

| Loan Maturity | Replace existing debt before payoff deadline | Bridge loan or bank refinance depending on stabilization |

| Recently Stabilized Property | Lock in long-term financing | Bank or agency loan |

| Property in Lease-Up | Improve occupancy before refinancing | Bridge loan followed by refinance |

| High Interest Rate Debt | Reduce borrowing costs | Bank refinance |

| Equity Extraction | Pull capital from increased value | Cash-out refinance |

| Mixed-Use or Complex Asset | Adjust structure to fit underwriting | Bridge or private loan |

Many Brooklyn properties transition from short-term financing into long-term loans once performance improves.

Short-term financing

Lease-up / improvements

Stronger income

New loan structure

Lower-cost financing

A common path in Brooklyn:

Refinance lenders focus on:

Rent-stabilized units and mixed-use components can influence underwriting.

We arrange refinancing for:

Request a confidential consultation to discuss pricing, market conditions, and sale strategy.

Commercial financing is available for multifamily buildings, mixed-use properties, development sites, retail assets, and industrial buildings. Each asset type is underwritten differently based on income, condition, and location.

Bridge loans are short-term and designed for speed and flexibility, often used for acquisitions or transitional properties. Bank financing typically offers lower rates and longer terms but requires stabilized income and more conservative underwriting.

Yes. If a property does not qualify for traditional bank financing, bridge loans or private lending may be available based on the asset’s value and the plan to improve performance.

Timing depends on the loan type. Bridge and private loans can close in a matter of weeks, while bank financing typically takes longer due to underwriting and documentation requirements.

No. We present financing options based on your property and objectives, and there is no obligation to proceed unless you decide to move forward with a specific loan.

Lenders evaluate factors such as net operating income, loan-to-value, property condition, and borrower experience. In some cases, particularly with bridge or private loans, the focus may be more on asset value and the exit strategy.