Brook Brokers arranges purchase financing for commercial real estate acquisitions in New York City, including multifamily, mixed-use, development, retail, and industrial properties.

Purchase financing must align with:

We match each deal with lenders familiar with the asset type and execution requirements.

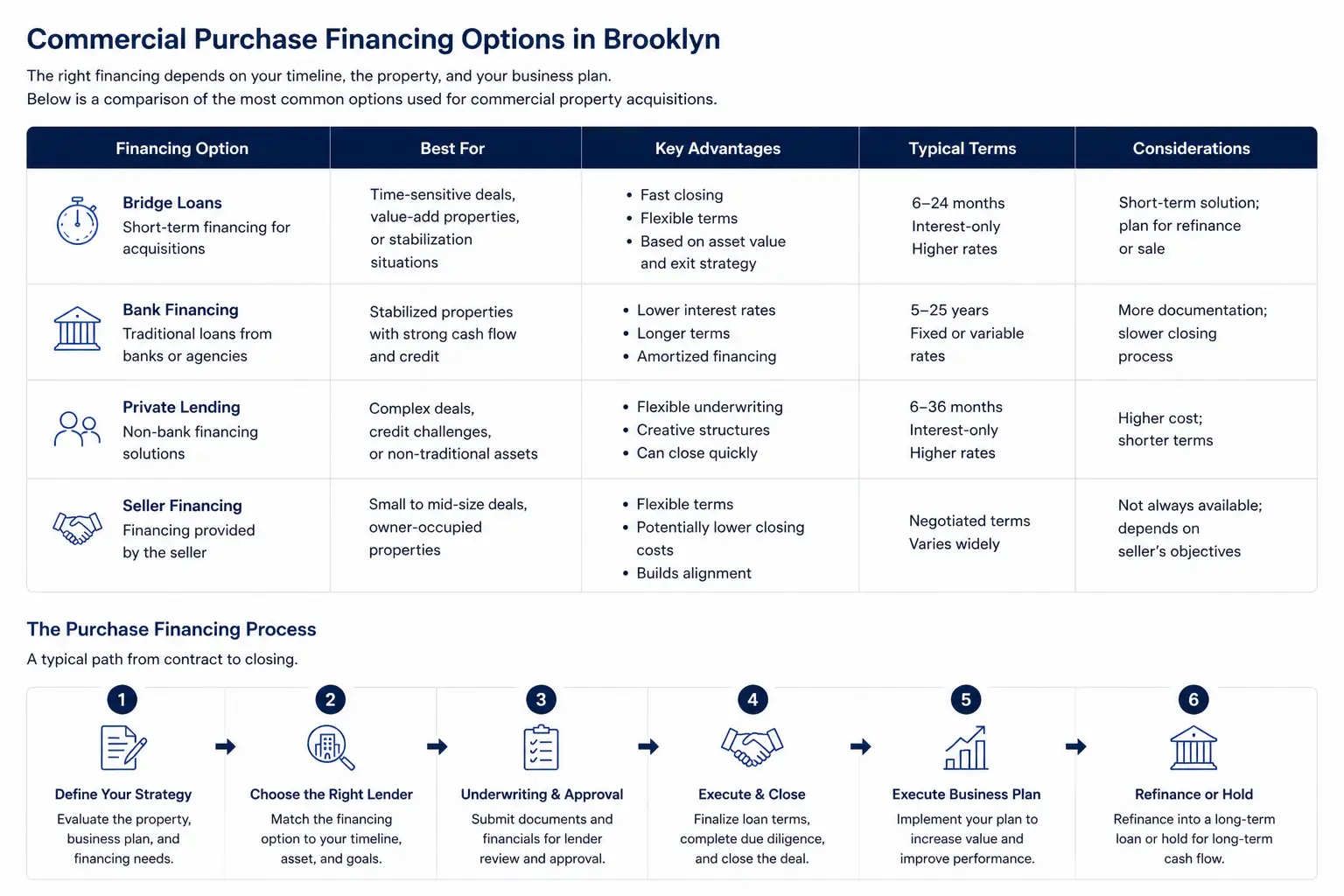

The right financing depends on your timeline, the property, and your business plan. Below is a comparison of the most common options used for commercial property acquisitions.

| Financing Option | Best For | Key Advantages | Typical Terms | Considerations |

|---|---|---|---|---|

|

Bridge Loans Short-term financing for acquisitions |

Time-sensitive deals, value-add properties, or stabilization situations |

|

6–24 months Interest-only Higher rates |

Short-term solution; plan for refinance or sale |

|

Bank Financing Traditional loans from banks or agencies |

Stabilized properties with strong cash flow and credit |

|

5–25 years Fixed or variable rates |

More documentation; slower closing process |

|

Private Lending Non-bank financing solutions |

Complex deals, credit challenges, or non-traditional assets |

|

6–36 months Interest-only Higher rates |

Higher cost; shorter terms |

|

Seller Financing Financing provided by the seller |

Small to mid-size deals, owner-occupied properties |

|

Negotiated terms Varies widely |

Not always available; depends on seller's objectives |

A typical path from contract to closing.

Evaluate the property, business plan, and financing needs.

Match the financing option to your timeline, asset, and goals.

Submit documents and financials for lender review and approval.

Finalize loan terms, complete due diligence, and close the deal.

Implement your plan to increase value and improve performance.

Refinance into a long-term loan or hold for long-term cash flow.

Depending on the deal, financing may include:

Bridge financing is often used when speed or repositioning is required, as outlined at /bridge-loans-brooklyn.

In Brooklyn, acquisition financing is influenced by:

These factors affect both leverage and lender selection.

We can review your acquisition and structure financing aligned with the property and your investment plan. A full overview of financing options is available at / Commercial-Financing-Brooklyn

Request a confidential consultation to discuss pricing, market conditions, and sale strategy.

Commercial financing is available for multifamily buildings, mixed-use properties, development sites, retail assets, and industrial buildings. Each asset type is underwritten differently based on income, condition, and location.

Bridge loans are short-term and designed for speed and flexibility, often used for acquisitions or transitional properties. Bank financing typically offers lower rates and longer terms but requires stabilized income and more conservative underwriting.

Yes. If a property does not qualify for traditional bank financing, bridge loans or private lending may be available based on the asset’s value and the plan to improve performance.

Timing depends on the loan type. Bridge and private loans can close in a matter of weeks, while bank financing typically takes longer due to underwriting and documentation requirements.

No. We present financing options based on your property and objectives, and there is no obligation to proceed unless you decide to move forward with a specific loan.

Lenders evaluate factors such as net operating income, loan-to-value, property condition, and borrower experience. In some cases, particularly with bridge or private loans, the focus may be more on asset value and the exit strategy.